U.S. Combined Heat and Power Systems Market

The U.S Combined Heat and Power (CHP) Systems Market is a rapidly growing sector of the U.S energy industry with immense potential to meet U.S energy needs in an efficient, cost-effective, and environmentally responsible manner. CHP systems use a single fuel source to generate both electricity and thermal energy, creating simultaneous savings in fuel costs, emissions reductions, and overall efficiency gains for U.S businesses and power plants.

Get Free Sample Copy of This Report -> https://www.persistencemarketresearch.com/samples/12958

CHP systems are employed across the U.S in various industries such as manufacturing, commercial buildings, hospitals, universities and colleges, government facilities, data centers, oil & gas production sites and other applications where thermal or cooling needs are present alongside the need for electricity generation. In addition to its utility in these diverse applications across U.S industries; CHP systems can also be used to supplement existing power grids as well as provide backup power during electrical outages or emergencies.

Key Companies-

- General Electric Company

- Caterpillar Inc.

- Clarke Energy Ltd.

- YANMAR America Corporation

- Kinsley Group

- Dresser-Rand Group, Inc.

- Burns & McDonnell Inc.

- Veolia Energy North America, LLC

- Unison Energy, LLC.

- IEM Power Systems, Inc.

- Dynamic Energy Solutions LLC

- Others

Complete Report Details@https://www.persistencemarketresearch.com/market-research/us-combined-heat-and-Power-systems-market.asp

Dominance of university laboratories prevails, followed by ISPs.

By application, over one-third share of the total market revenues will be occupied by university laboratories, i.e. over 36% by 2024-end. Internet service providers will also represent a remarkable revenue share of over 25% by the end of forecast period. Whereas, colos and server farms are expected to maintain steady growth throughout the assessment period.

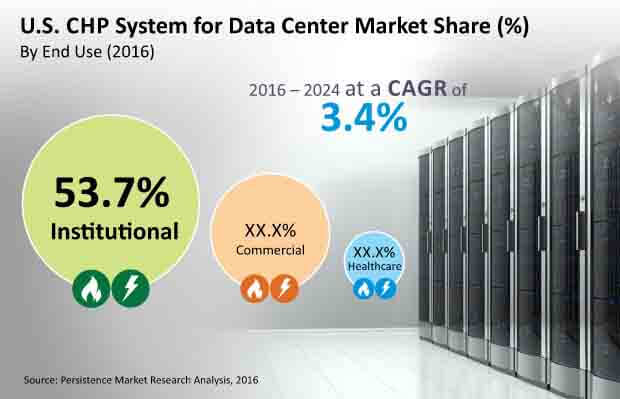

New system installations sway the U.S. market for CHP system – for data center.

Based on installation type, newly installed systems segment will continue to monopolize with over 81% share through 2024, gaining 130 BPS post-2016. Growth of retrofitting segment will however be relatively slower due to higher costs and associated complications.

Contact Us:

Persistence market research

Sales – sales@persistencemarketresearch.com

No comments:

Post a Comment